Inflation’s Impact on Your 2025 Budget: Save $500 Monthly

Understanding the impact of current inflation rates on your 2025 budget is crucial for financial stability, enabling proactive adjustments to spending habits to save a significant $500 monthly.

Navigating the financial landscape of the coming year requires foresight and strategic planning, especially when considering the impact of current inflation rates on your 2025 budget: adjusting spending to save $500 monthly.

For many, the persistent rise in prices has made managing household finances increasingly challenging, but with targeted adjustments, achieving significant savings is within reach.

Understanding the Current Inflation Landscape

Inflation refers to the general increase in prices and fall in the purchasing value of money. The current economic climate, marked by global supply chain disruptions, geopolitical tensions, and shifting consumer demands, has led to elevated inflation rates.

These rates directly influence the cost of everyday goods and services, from groceries and gasoline to housing and healthcare.

For 2025, economists predict that while inflation might temper slightly, it will likely remain above historical averages. This means that your dollar will continue to buy less than it did a few years ago, necessitating a proactive approach to personal finance.

Ignoring these trends could lead to a significant erosion of your purchasing power and a strain on your budget.

Key Inflationary Factors to Watch

- Energy Costs: Fluctuations in oil and gas prices directly affect transportation and utility bills.

- Food Prices: Agricultural disruptions and supply chain issues continue to drive up grocery costs.

- Housing Market: Rent and mortgage rates remain sensitive to economic policies and demand.

- Labor Costs: Rising wages, while beneficial for workers, can translate into higher prices for goods and services.

Understanding these underlying factors is the first step in preparing your budget. By recognizing where inflation hits hardest, you can anticipate potential increases in your expenses and begin to formulate a strategy for mitigation.

This foundational knowledge empowers you to make informed decisions rather than reacting to price shocks after they occur.

Assessing Your Current Spending Habits

Before you can effectively adjust your spending to save $500 monthly, a thorough assessment of your current financial outflow is essential. Many people are unaware of where their money truly goes each month, making it difficult to identify areas for reduction.

This assessment involves tracking every dollar spent over a period, typically one to three months, to establish a clear baseline.

Start by gathering all your financial statements: bank accounts, credit card statements, and any cash expenditures. Categorize your spending into fixed costs (rent, loan payments) and variable costs (groceries, entertainment, dining out).

The goal is to gain an objective view of your financial habits, free from assumptions or generalizations.

Tools for Tracking Expenses

- Budgeting Apps: Many apps like Mint, YNAB (You Need A Budget), or Personal Capital offer automated tracking and categorization.

- Spreadsheets: A simple spreadsheet can be highly effective for manual tracking, offering complete control over categories.

- Notebook and Pen: For those who prefer a more tactile approach, a dedicated notebook can help in logging daily expenses.

Once you have a clear picture of your spending, you can identify patterns and areas where money might be leaking unnecessarily. This initial audit is often eye-opening, revealing small, consistent expenses that accumulate into significant amounts over time.

It’s a crucial step that lays the groundwork for strategic adjustments.

Strategic Budget Adjustments for Inflation

With a clear understanding of both current inflation trends and your personal spending, the next step is to implement strategic budget adjustments. The objective is to find areas where you can reduce expenses without significantly compromising your quality of life, ultimately aiming to save $500 monthly.

This requires a thoughtful approach, distinguishing between needs and wants, and prioritizing financial goals.

Begin by targeting variable expenses, as these offer the most flexibility for immediate reduction. Dining out, entertainment, subscriptions, and impulse purchases are common areas where cuts can be made without drastically altering your lifestyle.

Consider negotiating fixed costs where possible, such as insurance premiums or internet bills.

Cutting Discretionary Spending

- Meal Planning: Reduce grocery waste and impulse buys by planning meals and sticking to a shopping list.

- Subscription Audit: Review all monthly subscriptions and cancel those you rarely use.

- DIY Entertainment: Opt for free or low-cost activities like parks, libraries, or home movie nights.

- Minimize Impulse Buys: Implement a 24-hour rule before making non-essential purchases.

Even small, consistent changes can add up quickly. For instance, bringing your lunch to work instead of buying it daily could save you $10-$15 per day, translating to $200-$300 a month. These micro-adjustments are often easier to sustain than drastic overhauls.

Optimizing Essential Expenses

While discretionary spending offers immediate opportunities for savings, optimizing essential expenses is equally vital for long-term financial health, especially with ongoing inflation. These are costs you can’t eliminate entirely, but you can often reduce them through savvy planning and negotiation.

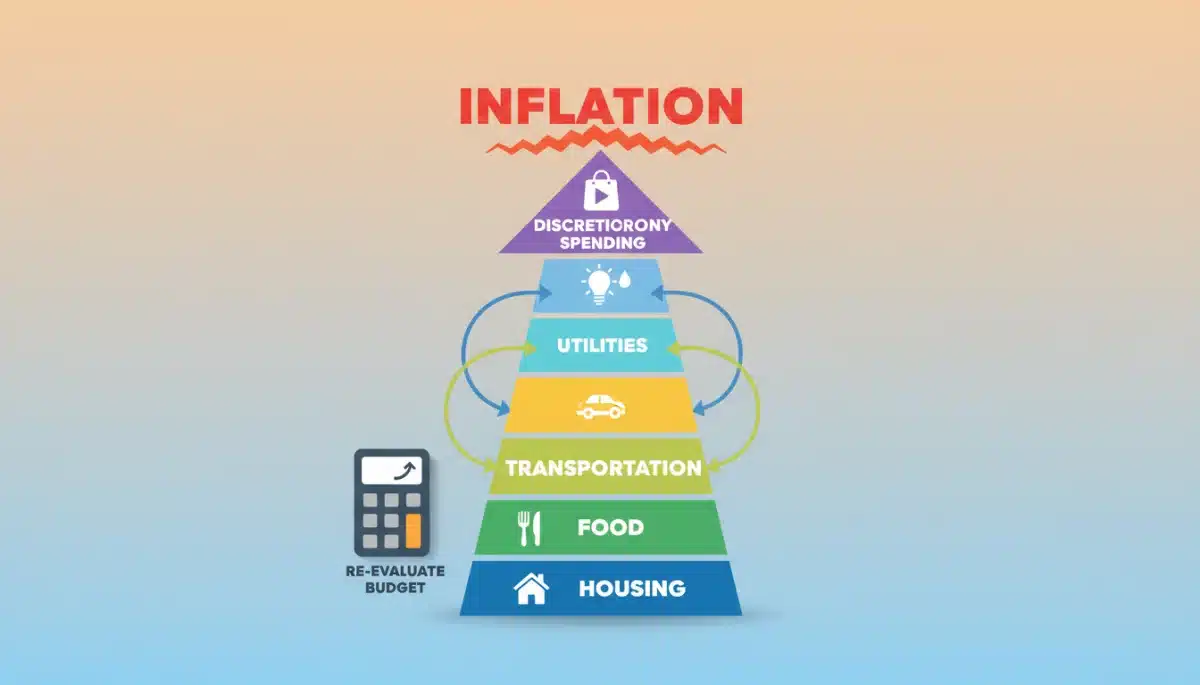

Housing, transportation, and utilities typically represent the largest portions of an essential budget.

For housing, consider ways to reduce energy consumption. For transportation, evaluate your commuting habits and explore alternatives. Food, a non-negotiable expense, can be managed more efficiently through careful planning and smart shopping.

These areas, while seemingly fixed, often hold hidden opportunities for significant savings.

Strategies for Essential Cost Reduction

- Energy Efficiency: Insulate your home, use smart thermostats, unplug unused electronics, and switch to energy-efficient appliances.

- Transportation Alternatives: Carpool, use public transport, bike, or walk more frequently. Combine errands to reduce fuel consumption.

- Smart Grocery Shopping: Buy in bulk when appropriate, utilize coupons and sales, choose generic brands, and cook more at home.

- Insurance Review: Shop around for better rates on auto, home, and health insurance annually.

Remember, every dollar saved in essential categories contributes directly to your $500 monthly goal. These adjustments might require more effort initially but yield consistent savings over time, providing a buffer against future inflationary pressures.

Leveraging Technology for Savings

In the digital age, technology offers powerful tools to help you manage your budget and identify savings opportunities, particularly when facing inflation. From automated budgeting apps to price comparison websites, these resources can streamline the process of tracking expenses and making smarter purchasing decisions.

Embracing technology can make the task of saving $500 monthly less daunting and more efficient.

Many personal finance apps now integrate with your bank accounts, automatically categorizing transactions and providing real-time insights into your spending. This immediate feedback allows for quicker adjustments and helps you stay on track with your budgeting goals.

Beyond tracking, technology can also help you find better deals and avoid overpaying for goods and services.

Tech Tools for Budget Optimization

- Price Comparison Apps/Extensions: Use tools like Honey, CamelCamelCamel, or Google Shopping to find the best deals online.

- Cash-Back and Rewards Apps: Utilize apps like Ibotta, Rakuten, or credit card rewards programs to get money back on purchases.

- Automated Savings Apps: Apps like Acorns or Digit can round up purchases or automatically transfer small amounts to savings.

- Bill Negotiation Services: Services like Trim or Billshark can negotiate lower rates on your monthly bills.

By strategically employing these technological aids, you can automate much of the saving process, making it easier to identify and capture savings that might otherwise go unnoticed. This not only helps meet your $500 monthly target but also fosters better long-term financial habits.

Building Financial Resilience for 2025 and Beyond

Adjusting your budget to save $500 monthly in response to inflation is not just about immediate relief; it’s about building long-term financial resilience. The strategies discussed, from understanding inflation to optimizing spending, contribute to a stronger financial foundation.

This resilience is crucial for navigating future economic uncertainties and achieving broader financial goals.

Beyond immediate savings, consider how these adjustments can free up funds for an emergency savings account, debt reduction, or investments. A robust emergency fund, ideally covering 3-6 months of living expenses, is your first line of defense against unexpected costs or income disruptions.

Reducing high-interest debt can further alleviate financial pressure and free up more monthly cash flow.

Long-Term Financial Strategies

- Emergency Fund: Prioritize building a substantial emergency savings account to cover unforeseen expenses.

- Debt Reduction: Focus on paying down high-interest debts, such as credit card balances, to improve your financial health.

- Investment Planning: Explore low-cost investment options to grow your wealth over time and combat inflation’s effects.

- Diversify Income Streams: Consider side hustles or opportunities to earn additional income to supplement your main source.

The discipline gained from actively managing your budget during inflationary times will serve you well in all aspects of your financial life. It instills habits of mindfulness and planning that are invaluable for achieving financial independence and security.

Monitoring and Adapting Your Budget

Creating a budget and making initial adjustments are significant steps, but continuous monitoring and adaptation are just as important, especially in an ever-changing economic climate. Inflation rates and personal circumstances can shift, requiring your budget to be flexible and responsive.

Regularly reviewing your financial plan ensures it remains relevant and effective in helping you save $500 monthly.

Set aside time each month, perhaps a specific day, to review your spending and savings. Compare your actual expenditures against your budgeted amounts. Identify any discrepancies and understand why they occurred. This iterative process allows you to refine your budget, making it more accurate and sustainable over time.

Don’t be afraid to make changes as your financial situation evolves.

Tips for Ongoing Budget Management

- Monthly Review: Dedicate an hour each month to review your budget and financial statements.

- Adjust as Needed: Life happens; be prepared to modify your budget to reflect new income, expenses, or financial goals.

- Set Realistic Goals: While saving $500 is a great target, ensure your overall budget remains achievable to avoid burnout.

- Celebrate Progress: Acknowledge your achievements, big or small, to stay motivated on your financial journey.

By consistently monitoring and adapting your budget, you transform it from a rigid set of rules into a dynamic financial tool. This proactive approach ensures you remain in control of your finances, effectively mitigating the impact of inflation and steadily progressing towards your savings goals.

| Key Strategy | Brief Description |

|---|---|

| Assess Spending | Track all expenses for 1-3 months to identify spending patterns and areas for reduction. |

| Adjust Discretionary Spending | Reduce non-essential costs like dining out, subscriptions, and impulse purchases. |

| Optimize Essential Expenses | Implement energy efficiency, smart grocery shopping, and review insurance rates. |

| Leverage Technology | Utilize budgeting apps, price comparison tools, and cash-back programs to find savings. |

Frequently Asked Questions About Budgeting in Inflation

Inflation reduces the purchasing power of money, meaning your dollars buy less. This leads to higher costs for everyday necessities like food, fuel, and housing, effectively shrinking your disposable income if your wages don’t keep pace. It necessitates re-evaluating spending to maintain financial stability.

Common areas for significant savings include reducing dining out, canceling unused subscriptions, optimizing grocery spending through meal planning, and cutting down on discretionary purchases like new gadgets or entertainment. Even small, consistent cuts in these categories can quickly add up.

Yes, it is realistic, but it requires diligent tracking, strategic adjustments, and sometimes making difficult choices. By combining cuts in discretionary spending with optimization of essential expenses and leveraging financial tools, many individuals can achieve or even exceed this savings goal.

It’s advisable to review your budget at least once a month. This allows you to track your progress, identify any overspending, and make necessary adjustments based on changes in income, expenses, or the economic environment. Regular reviews ensure your budget remains effective and relevant.

Technology offers invaluable tools for budget management. Apps can automate expense tracking, provide spending insights, and help you find deals. Price comparison websites ensure you pay fair prices, while automated savings tools can make saving effortless, all crucial for combating inflation’s impact.

Conclusion

The persistent challenge of inflation demands a proactive and adaptable approach to personal finance. Understanding the impact of current inflation rates on your 2025 budget: adjusting spending to save $500 monthly is not merely an aspiration but a necessity for financial stability. By meticulously assessing spending, strategically cutting discretionary costs, optimizing essential expenses, and leveraging modern financial tools, individuals can effectively navigate the economic headwinds. Building financial resilience through consistent monitoring and smart adjustments ensures that your budget remains a dynamic tool, empowering you to achieve significant savings and secure your financial future in an evolving economic landscape.