2025 Social Security COLA: Impact on Your Finances

The 2025 Social Security Cost-of-Living Adjustment (COLA) is a vital adjustment designed to help beneficiaries maintain purchasing power against inflation, directly impacting their financial stability and budgeting for the upcoming year.

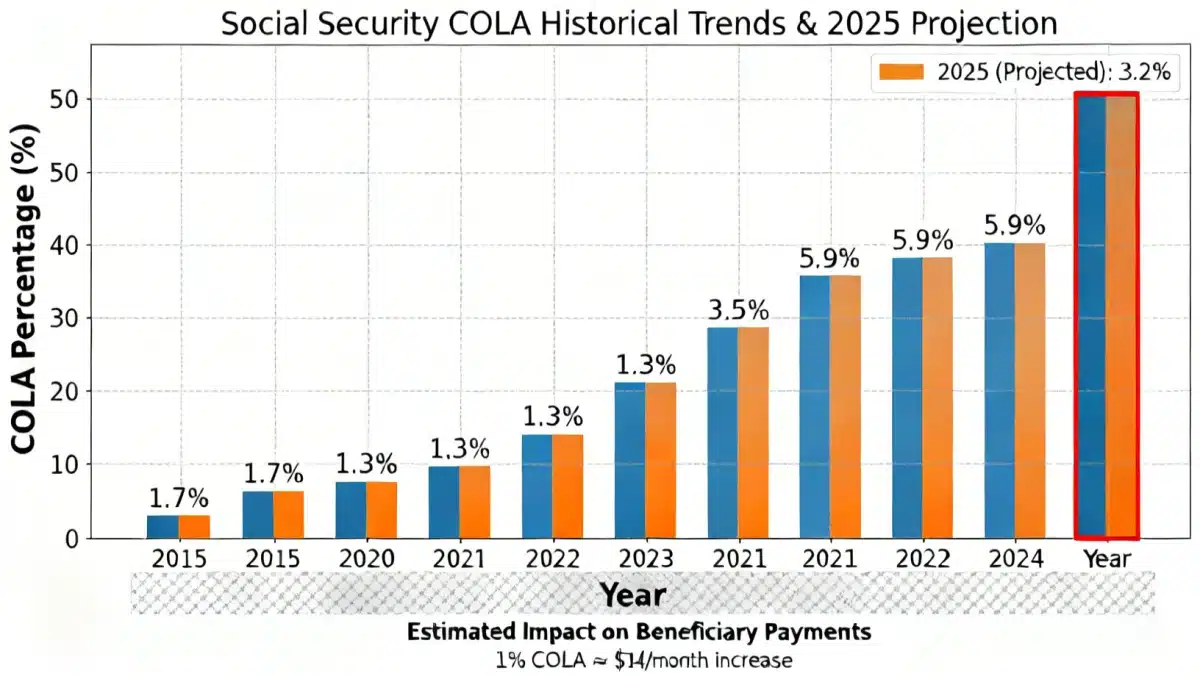

For millions of Americans, understanding the 2025 Social Security Cost-of-Living Adjustment (COLA) and its financial impact is not merely an academic exercise; it’s a critical component of personal financial planning. This annual adjustment is designed to help Social Security beneficiaries keep pace with the rising cost of living, ensuring their benefits retain their purchasing power amidst inflationary pressures. As we approach 2025, anticipating the COLA’s specifics and its broader economic implications becomes increasingly important for retirees, disabled individuals, and survivors who rely on these payments.

The mechanics of Social Security COLA: how it’s calculated

The Social Security Cost-of-Living Adjustment, or COLA, is a crucial mechanism that ensures the financial stability of millions of Americans. It’s not a discretionary decision but rather a calculation driven by specific economic indicators, primarily inflation. Understanding this process is key to appreciating how your future benefits might change and what that means for your financial outlook.

The Social Security Administration (SSA) determines the COLA based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This particular index measures the average change over time in the prices paid by urban wage earners and clerical workers for a market basket of consumer goods and services. By using the CPI-W, the SSA aims to reflect the inflation experienced by a significant portion of its beneficiaries, ensuring that benefit adjustments are relevant to their actual living costs.

The role of the CPI-W in COLA determination

- Measurement Period: The SSA compares the average CPI-W for the third quarter (July, August, and September) of the current year with the average CPI-W for the third quarter of the last year in which a COLA was enacted.

- Percentage Increase: The percentage increase between these two periods directly translates into the COLA percentage for the following year. If there’s no increase, or a decrease, there’s no COLA for that year.

- No Decrease: Social Security benefits never decrease due to a negative CPI-W. If inflation is negative, the COLA is zero, meaning benefits remain the same.

This methodology provides a standardized and transparent way to adjust benefits. While some argue that the CPI-W may not fully capture the specific spending patterns of seniors, particularly healthcare costs, it remains the congressionally mandated index for COLA calculations. The consistency of this method allows for a predictable framework, even if the exact percentage varies year to year.

In conclusion, the COLA calculation is a direct response to inflationary trends, specifically those captured by the CPI-W. This mechanism is fundamental to Social Security’s promise to provide a safety net that adapts to economic realities, helping beneficiaries maintain their purchasing power in an ever-changing financial landscape.

Forecasting the 2025 COLA: expert predictions and economic indicators

Predicting the exact 2025 Social Security COLA is a complex task, as it hinges on inflation data that won’t be fully available until late 2024. However, economists and financial analysts regularly offer projections based on current economic trends and historical patterns. These forecasts provide valuable insights for beneficiaries to begin their financial planning, even if they are subject to change.

Several key economic indicators are closely watched for their influence on the CPI-W, and consequently, the COLA. Energy prices, food costs, and housing expenses are primary drivers of inflation and tend to have a significant impact on the CPI-W. Labor market conditions, wage growth, and global supply chain stability also play a role, as they can either fuel or dampen inflationary pressures.

Factors influencing COLA projections

- Inflation Trends: Sustained inflation, particularly in essential goods and services, points towards a higher COLA. Conversely, cooling inflation suggests a lower adjustment.

- Federal Reserve Policy: The Federal Reserve’s monetary policies, such as interest rate adjustments, influence economic activity and inflation rates, indirectly affecting the COLA.

- Global Economic Events: Geopolitical events, international trade dynamics, and global supply chain disruptions can all create inflationary pressures that reflect in the CPI-W.

Early expert predictions for the 2025 COLA often involve analyzing current inflation rates and projecting them forward. While these are not guarantees, they offer a reasonable starting point for beneficiaries to consider. For instance, if inflation remains elevated in the first half of 2024, it’s more likely that the 2025 COLA will be higher than if inflation significantly cools down.

The ongoing economic environment, characterized by evolving inflationary pressures and policy responses, makes precise COLA forecasting challenging. Nevertheless, staying informed about these expert predictions and the underlying economic indicators allows beneficiaries to make more informed decisions about their financial future.

Direct financial impact: what a 2025 COLA means for your benefits

The announcement of the 2025 Social Security COLA will have a direct and tangible impact on the monthly benefits received by millions of Americans. While the percentage might seem small, even a modest adjustment can significantly affect a beneficiary’s budget and purchasing power throughout the year. Understanding this direct impact is crucial for effective financial management.

When the COLA is applied, all Social Security benefits, including retirement, disability, and survivor benefits, will increase by the announced percentage. This means that if you currently receive a certain amount, that amount will be multiplied by (1 + COLA percentage) to determine your new monthly payment. For example, a 3% COLA on a $1,800 monthly benefit would result in an extra $54 per month, totaling $648 annually.

Calculating your increased benefit

To calculate your estimated new benefit, simply multiply your current monthly benefit by the COLA percentage (expressed as a decimal) and add that amount to your current benefit. This straightforward calculation allows you to quickly see the potential increase in your income and adjust your budget accordingly.

- Budgeting: An increased benefit can provide much-needed relief from rising costs, allowing for better budgeting for essentials like food, housing, and utilities.

- Discretionary Spending: For some, a COLA increase might free up funds for discretionary spending, improving quality of life.

- Healthcare Costs: While benefits increase, it’s important to remember that Medicare Part B premiums are often deducted directly from Social Security checks. An increase in these premiums could offset some of the COLA benefit.

It’s important to recognize that the COLA is designed to maintain, not increase, purchasing power. While your dollar amount goes up, the intention is for that increase to simply cover the higher costs of goods and services. Therefore, while a COLA is always welcome, it’s essential to view it in the context of the broader economic environment and your personal financial situation.

In essence, the 2025 COLA will directly translate into a higher monthly payment for beneficiaries. This adjustment is a vital tool for ensuring that Social Security continues to provide a meaningful safety net, helping individuals navigate the financial challenges posed by inflation.

Indirect consequences: Medicare premiums and taxation

While the 2025 Social Security COLA directly boosts your benefit payments, it’s crucial to understand that it can also trigger indirect consequences, particularly concerning Medicare premiums and the potential taxation of your Social Security benefits. These interconnected financial factors require careful consideration for a complete picture of your financial well-being.

One of the most significant indirect impacts of a COLA is on Medicare Part B premiums. By law, increases in Part B premiums are often constrained by the COLA, meaning that for many beneficiaries, their Part B premium increase cannot exceed their COLA increase. However, if your income is above certain thresholds, you may be subject to the Income-Related Monthly Adjustment Amount (IRMAA), which means paying higher Part B and Part D premiums. A higher COLA could, for some, push their modified adjusted gross income (MAGI) into a higher IRMAA bracket.

Understanding the tax implications of COLA

Another important consideration is the potential for your Social Security benefits to become taxable. If your combined income (adjusted gross income + non-taxable interest + one-half of your Social Security benefits) exceeds certain thresholds, a portion of your Social Security benefits may be subject to federal income tax. A higher COLA, by increasing your overall income, could push you past these thresholds or increase the taxable portion of your benefits.

- Tax Thresholds: For 2024, if your combined income is between $25,000 and $34,000 for an individual, up to 50% of your benefits may be taxable. Above $34,000, up to 85% may be taxable. These thresholds are not indexed for inflation, making them more likely to be met over time.

- State Taxes: Some states also tax Social Security benefits. It’s essential to check your state’s specific rules, as a COLA increase could also affect your state tax liability.

Therefore, while a COLA increase is generally positive, it’s vital to assess its impact on your overall financial situation, taking into account potential increases in Medicare premiums and the possibility of higher tax obligations. Proactive planning and consulting with a financial advisor can help mitigate any adverse effects and ensure you maximize your net benefits.

In summary, the 2025 COLA’s influence extends beyond just your monthly check. It’s a complex interplay with Medicare costs and tax liabilities, underscoring the need for a holistic financial perspective.

Strategic planning for beneficiaries: maximizing your 2025 COLA

For Social Security beneficiaries, strategic planning around the 2025 COLA is essential to maximize its positive impact and minimize any potential drawbacks. While the COLA is an automatic adjustment, how you manage your finances in response can significantly affect your overall financial health. This involves reviewing your budget, understanding potential tax implications, and exploring other income streams.

One of the primary steps is to re-evaluate your household budget. With a potentially increased monthly benefit, you have an opportunity to adjust your spending habits or allocate funds more effectively. This could mean increasing your savings, paying down debt, or simply having more flexibility for daily expenses. It’s also a good time to review your fixed costs, such as utilities and insurance, to ensure you’re getting the best value.

Key strategies for COLA optimization

- Budget Reassessment: Update your budget to reflect the new benefit amount, prioritizing essential expenses and identifying areas for potential savings or increased discretionary spending.

- Tax Planning: Consult with a tax professional to understand how the COLA might affect your federal and state tax liability, especially concerning the taxation of Social Security benefits and Medicare IRMAA thresholds.

- Healthcare Cost Review: Investigate if your Medicare Part B or D premiums will change. Consider exploring Medicare Advantage plans or prescription drug plans that might offer better value for your specific health needs.

- Emergency Fund: If your emergency fund is not fully stocked, consider directing a portion of your COLA increase towards building or replenishing it.

Beyond budgeting, consider how the COLA might fit into your broader retirement income strategy. If you have other sources of income, such as pensions, investments, or part-time work, the COLA can complement these, providing a more robust financial foundation. It’s also an opportune moment to review your investment portfolio, if applicable, to ensure it aligns with your risk tolerance and financial goals.

Ultimately, strategic planning for the 2025 COLA means taking a proactive approach to your finances. By understanding the adjustment’s potential effects and making informed decisions, beneficiaries can optimize their financial situation and enhance their peace of mind.

The broader economic context: inflation, wages, and the labor market

The 2025 Social Security COLA doesn’t exist in a vacuum; it’s a direct reflection of the broader economic environment, particularly the interplay between inflation, wages, and the labor market. Understanding this wider context provides a deeper appreciation for how the COLA is determined and its significance beyond individual benefit checks. The economic forces at play shape the cost of living and, consequently, the need for benefit adjustments.

Inflation, as measured by the CPI-W, is the most direct driver of the COLA. High inflation means that the cost of goods and services is rising rapidly, eroding purchasing power. The COLA’s purpose is to counteract this erosion, ensuring that beneficiaries can still afford essential items. The persistent inflation experienced in recent years has highlighted the critical role of COLA in protecting vulnerable populations.

Interconnected economic factors

- Wage Growth: Strong wage growth in the labor market can contribute to inflationary pressures, as higher labor costs are often passed on to consumers through increased prices.

- Labor Market Health: A robust labor market, characterized by low unemployment and high demand for workers, can also lead to increased consumer spending, further fueling inflation. Conversely, a weakening labor market might temper inflationary pressures.

- Supply Chain Dynamics: Global supply chain issues, such as those seen during the pandemic, can restrict the availability of goods, leading to higher prices and contributing to inflation.

Government fiscal policies and central bank monetary policies, such as interest rate adjustments by the Federal Reserve, also play a crucial role. These policies aim to manage inflation and maintain economic stability, which in turn influences the COLA calculation. For instance, aggressive interest rate hikes might cool inflation, potentially leading to a lower COLA in subsequent years, though this also carries risks for economic growth.

The ongoing economic narrative, with its focus on inflation control and labor market stability, directly informs the expectations for the 2025 COLA. By observing these macroeconomic trends, individuals can gain a better perspective on the potential adjustment and its implications for their financial planning.

Ultimately, the 2025 COLA is more than just a number; it’s a barometer of the nation’s economic health and a testament to the ongoing effort to protect the financial well-being of Social Security beneficiaries against the backdrop of dynamic economic forces.

Preparing for future COLA adjustments: long-term financial resilience

While the focus is currently on the 2025 Social Security COLA, adopting a long-term perspective on these adjustments is vital for building lasting financial resilience. COLA is an annual event, and understanding how to prepare for future changes can empower beneficiaries to navigate their financial journey with greater confidence and security. This involves proactive planning that extends beyond immediate reactions to each year’s announcement.

One key aspect of long-term preparation is to avoid relying solely on Social Security benefits for your entire retirement income. While COLA helps benefits keep pace with inflation, having diversified income streams—such as personal savings, pensions, or investment portfolios—provides a stronger financial buffer. This diversification can help cushion against years with low or no COLA, or unexpected expenses.

Building long-term financial stability

- Diversify Income: Explore various income sources beyond Social Security to reduce dependency and enhance overall financial security.

- Maintain a Robust Emergency Fund: A well-funded emergency savings account can cover unexpected costs, reducing the reliance on a COLA increase for unforeseen expenses.

- Regular Financial Reviews: Periodically review your budget, investments, and overall financial plan to adapt to changing economic conditions and COLA adjustments.

- Stay Informed: Keep abreast of economic forecasts and Social Security policy discussions to anticipate potential changes to future COLA calculations or benefit structures.

Furthermore, understanding the historical trends of COLA and the economic factors that influence it can help in setting realistic expectations for future adjustments. While high inflation years might bring significant COLAs, periods of stable or low inflation will result in smaller increases. Factoring these possibilities into long-term financial projections is a prudent approach.

Engaging with financial advisors who specialize in retirement planning can also be immensely beneficial. They can help you create a comprehensive financial strategy that accounts for future COLA adjustments, potential changes in healthcare costs, and tax implications, ensuring your financial plan remains robust and adaptable over time.

In conclusion, preparing for future COLA adjustments is about fostering long-term financial resilience. By diversifying income, building savings, and staying informed, beneficiaries can ensure their financial well-being is not solely dependent on annual Social Security increases, but rather on a well-rounded and adaptable financial strategy.

| Key Point | Brief Description |

|---|---|

| COLA Calculation | Determined by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from Q3 data. |

| Direct Impact | Increases monthly Social Security benefits, aiming to preserve purchasing power against inflation. |

| Indirect Impact | Can affect Medicare Part B premiums and the federal taxation of Social Security benefits. |

| Strategic Planning | Beneficiaries should budget, tax plan, and diversify income to maximize COLA’s benefits. |

Frequently asked questions about the 2025 Social Security COLA

The COLA, or Cost-of-Living Adjustment, is designed to help Social Security and Supplemental Security Income (SSI) beneficiaries maintain their purchasing power. It aims to offset the effects of inflation, ensuring that the value of their benefits doesn’t erode over time due to rising costs for goods and services.

The 2025 COLA will be calculated based on the increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the average CPI-W for the third quarter of 2024 will be compared to the average for the third quarter of the last year a COLA was paid.

Yes, the 2025 COLA can affect Medicare Part B premiums. While the ‘hold harmless’ provision protects many from premium increases that exceed their COLA increase, higher incomes due to COLA could potentially push some beneficiaries into higher Income-Related Monthly Adjustment Amount (IRMAA) brackets.

Yes, an increase from the 2025 COLA could potentially make a larger portion of your Social Security benefits subject to federal income tax. This happens if the increase pushes your ‘combined income’ (adjusted gross income plus non-taxable interest plus half your Social Security benefits) above certain thresholds.

The official 2025 Social Security COLA is typically announced by the Social Security Administration in October of the preceding year, once the third-quarter CPI-W data becomes fully available. Beneficiaries will usually see the adjustment reflected in their December benefits, paid in January.

Conclusion

The 2025 Social Security Cost-of-Living Adjustment is a fundamental aspect of financial planning for millions of Americans who rely on these benefits. From its intricate calculation based on the CPI-W to its direct impact on monthly checks and indirect effects on Medicare premiums and taxation, understanding the COLA is paramount. Proactive financial strategies, including budgeting, tax planning, and diversification of income, will empower beneficiaries to maximize the benefits of the COLA and build greater long-term financial resilience. Staying informed about economic trends and seeking professional advice can further enhance preparedness, ensuring that Social Security continues to provide a vital safety net in an evolving economic landscape.